For subscribers only

Subscribe now to read this post and also gain access to Jom’s full library of content.

Subscribe now Already have a paid account? Sign in

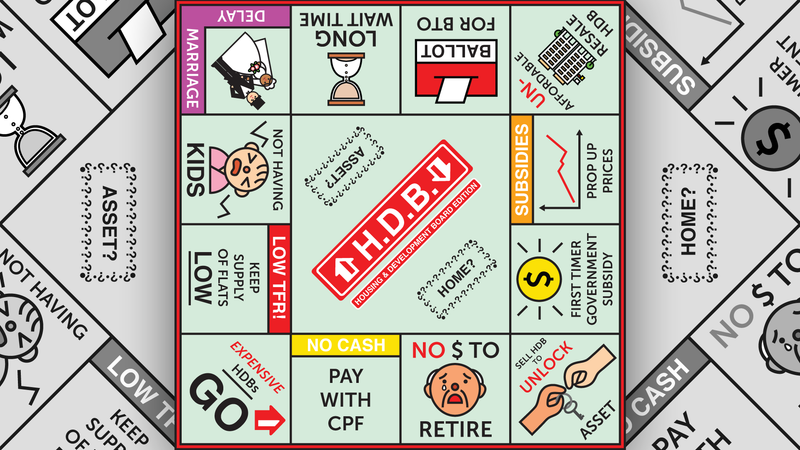

How has Singapore’s public housing model evolved since independence? In analysing the roots of this model and examining the factors contributing to the current public housing crisis, this essay argues that a revision of the original Housing and Development Board programme is vital moving forward.

Subscribe now to read this post and also gain access to Jom’s full library of content.

Subscribe now Already have a paid account? Sign in

Precarity, gossip, aspirations, and “Melayu makan Melayu”.

The way your group splits its food bill reveals much about your particular history, informal rules, and sense of fairness.

The migratory history of a remarkable micro-community from south India.

By negotiating our use of shared space directly, while being mindful of others’ needs, we can nurture a compassionate, empathetic society

On March 25th, the Harvard Club of Singapore (HCS) announced that Dr Kanwaljit Soin had won its 2026 Fellow Award. This is her acceptance speech, which Jom felt deserved a wider audience. We’re grateful to Dr Soin for allowing us to republish it.

Please click on the link sent to your e-mail to login to your account.